Rich Sis™ Guides

So, you’re ready to get a handle on this credit thing, but don’t know where to start? Bankable’s got you covered.

Your credit is essential to your future. Over the course your lifetime, great credit can save your tens, or even hundreds, of thousands of dollars.

By mastering the credit game, you’ll take charge of your finances. Let’s get started.

Credit is the ability to receive a good or service immediately by making a promise to pay over time (or at some future date).

It can be in the form of a loan (like a car loan or mortgage), a revolving credit line (like a credit or store card), or some combination of the two.

The savvy use of credit is essential to a successful long-term financial plan. By building and maintaining a strong credit profile, you can save tens of thousands of dollars on major purchases over your lifetime.

Your credit score is used by lenders, insurers, and even employers to evaluate your trustworthiness and employability.

Is it fair? Not really.

Even so, if you want to get ahead and secure your future, mastering the credit game will give you an edge in everything – from job hunting to renting that luxury apartment you love.

Can’t I Just Use Cash (Avoid the Credit Trap)?

This is a common question, and some financial “gurus” advise their readers to live by this.

Cash is King, but credit is Queen.

Having excellent credit makes large purchases (like a home, for example) more accessible to most people. Unless you have a few hundred thousand dollars saved up, buying a home without a mortgage could prove impossible.

Many Americans don’t save that kind of money in a lifetime, let alone over the course of a few years. Credit makes it possible to make strategic purchases that can increase your net worth and improve your life.

A huge savings goal can take several years to achieve. Can you put off your financial goals – buying a home, going to college – for a decade or more while you work to save enough?

If you’re an entrepreneur, credit provides the opportunity to take short-term “loan” to pay for supplies or other essentials.

Your credit report is a list that tracks your credit-related activity over several years. The three major credit bureaus each have their own version of this report, and calculate their own score based on the information reported to them.

Your credit report includes identifying information, including

Your credit score is a numeric calculation of your creditworthiness based on the information in your credit report. This number is used by lenders, vendors, and employers to decide whether to do business with you.

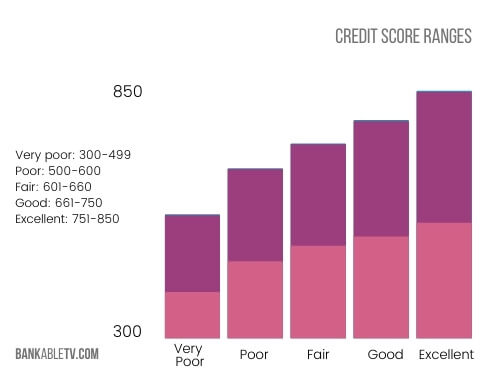

Credit scores range between 300-850.

There are several different credit scoring models, and different industries use different versions when evaluating your credit history. The most well-known are the Fair Isaac Corporation (FICO) and the Vantage score. More on each of these later.

A FICO score of 700+ is considered good, with anything over 750 being considered excellent credit.

Higher scores will qualify you for the best interest rates and most favorable loan terms in almost any borrowing situation.

The average credit score is around 700, with scores tending to increase with age.

Having a very good (or better) credit score signals to lenders that you’re pretty financially responsible, and not likely to default on financial obligations.

Credit scores aren’t as mysterious as most people believe. Each scoring agency has a set of parameters they use to calculate scores. Knowing the key elements that impact a credit score can help you build (or rebuild) a score that works for you.

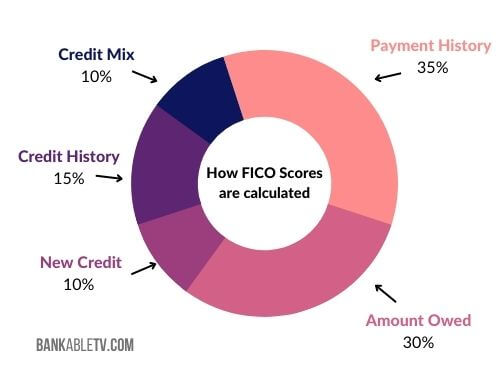

Your scores are based on the following factors:

The factors that make up your credit score calculation are very specific. Some you can control; others are created by default based on the age of your credit history.

The largest part of your credit score is your payment history. The more consistent you are about paying every bill on time, the better your score.

In addition to avoiding late fees and accruing interest, paying on time will help you build an attractive history that appeals to lenders.

Making just one payment 30 days late can cause your score to drop by more than 50-100 points.

Worse still, the late payment will remain on your credit report for the next seven years. Avoid late payments at all costs, whenever possible.

The 2nd largest chunk of your score is the amount owed on your credit obligations. This amount is called your utilization ratio, and the higher the amount of credit you use, the more it hurts your score.

Utilization rate is calculated by:

Let’s say you owe $72,000 on your credit cards.

If you have $100,000 in available credit, your utilization rate is 72%. Not good.

What is a good utilization rate?

Keeping your balances under 30% of your available credit is a good start.

The ideal utilization ratio is under 10% if you want to maximize your credit score.

Lenders love consistency. The longer your credit history, the better it is for your score. There’s little you can do to control this element of your credit score.

Once you open a credit account, never close it. Make small purchases on your oldest accounts to ensure there’s activity to keep them open.

Your credit mix accounts for 10% of your credit score. The credit bureaus will look at how many different types of credit accounts you have (revolving credit, charge accounts, installment and mortgage loans, etc.) when evaluating your history.

This won’t have a huge impact on your score, but lenders like to see that you can responsibly manage more than one type of account.

Lenders take into account the amount of newly acquired credit on your reports as well. Lots of new accounts or inquiries (applications for new credit) can signal that you’re facing financial hardship.

Keep your number of new accounts to a minimum, and you’ll maximize your credit score.

As you can see, more than 80% of your credit is easy to control.

The foundation of an effective credit strategy is building a flawless payment history and keeping an eye on how much you spend.

You should check your credit reports at least twice each year.

According to the Federal Trade Commission, about 20% of people have at least one error on their credit reports. Credit reporting inaccuracies can cause your score to drop, so staying on top of the information lenders see could save you money.

Every American is entitled to one free copy of your credit report from each of the credit bureaus each year.

To access your reports, visit AnnualCreditReport.com.

Now that you’re armed with the credit basics, you can make an effective plan to level up your credit scores. Check out the tips and resources below to level up your credit game.

No matter where you’re starting, your credit success is in your hands. Once you’ve checked your credit reports know where you stand, it’s time to develop a strategy to improve.

If you’re brand new to credit, your goal should be to qualify for high-quality credit accounts and build a great payment history.

If you’re rebuilding after a stumble, you’ll need to maximize positive credit information and work to remove derogatory accounts.

Setting clear goals is the first step to success. By deciding that you want to improve your credit, you’ll dedicate your energy to this achievement.

Your credit growth is a private, individual experience. Set goals that you feel work for you.

Starting with a 500? Perhaps you want to move up to a 620. If you’ve got a 700, you can shoot for a 50-point jump to start getting those prime credit offers.

Your goal is completely up to you; make it something that inspires you to do the work.

Next up, it’s time to review your report and decide which accounts are best for improving your credit profile.

If you only have entry level credit cards, make a plan to level up to higher tier cards & larger credit lines. Decide what steps you can take with your current accounts to boost your credit score, and take action.

Since your payment history makes up 35% of your credit score, it makes sense to focus a lot of your effort there. Avoid late payments at all costs.

If your finances take a turn, be sure to reach out to your creditors quickly to make arrangements and ask for support. If you have a strong relationship with them, you may be able to avoid late fees, APR increases and 30-day late payment marks on your report.

The length of your credit history and the average age of your accounts make up 20% of your credit score.

Once you open a credit account, keep it open and in good standing as long as possible. If you’ve have any credit cards that carry high interest and fees, pay them off and cancel those accounts immediately. Your score will take a hit, but they won’t be able to continue to suck you dry.

Predatory credit cards and lenders are the only accounts you should be getting rid of. As your score increases, replace these cards with higher-tier cards that offer you better terms and fewer fees.

Once you’ve gotten some quality cards, take a break from applying for new credit accounts. Keep new account inquiries to no more than one (1) per year.

Once you’ve developed a new credit baseline, make it a habit to monitor your credit reports & scores.

Review your reports from each credit bureau at least once per quarter (every 3 months). Request that outdated information be removed (old addresses, employers, etc). The more vigilant you are about your credit, the less likely an error will slip through the cracks.

Your credit health is in your hands.

Get a secured card. If your credit file is thin (or nonexistent), starting with a secured credit card can get you on the right track.

Secured credit cards require a deposit to open. That deposit is used as collateral to “secure” your credit line. In case the bill goes unpaid, the credit card company recoups the money owed from the secured account.

Secured cards are good for new credit builders because they usually have low limits. Some offer credit education to their members.

Once you’ve gotten used to handling your credit, consider ask to have your card “graduated” to an unsecured account.

Apply for a credit builder loan. A credit builder loan is a useful tool for those new to building credit. They’re usually offered by small banks and credit unions. The financial institution won’t use your credit score as the most import part of your application like most lenders would.

Once you’re approved, the money from the loan is held in an account until you’ve paid off the loan in full.

You receive access to the funds after the loan is paid. It helps build your credit by reporting your monthly payments to one or more of the credit bureaus.

Become an authorized user on a credit star’s card. If you want to supercharge your credit building, becoming an authorized user on an established credit line can help.

Authorized users are added to existing accounts by a friend or family member. When this happens, an additional card is issued in the your name, and you can use that card for purchases. The account holder then becomes responsible for repayment of any charges made by you.

That’s not what makes this strategy powerful, though. A credit card holder who decides to help an AU can add them to their account and never give them the card.

That way, the authorized user get the credit benefits of the account holder’s credit and payment history, but there’s no risk of the card being misused.

If you have access to someone with great credit who’d be willing to give your credit a boost, run, don’t walk to get added on.

Dispute inaccurate information. The credit bureaus estimate that around 20% of all credit reports have inaccuracies. That number is likely much higher, but inaccuracies are usually only caught if a person checks their own credit files.

Make it a habit to check your credit report with all 3 bureaus at least twice a year.

If you find incorrect or outdated information, contact the bureau and start the dispute process.

Pay down cards with high balances. The closer your balance is to your credit card limit, the worse it is for your credit score. By paying down high balances, you’ll improve your utilization and debt-to-income ratios, both of which make you a more attractive borrower.

Keep utilization under 10%. Once you’ve paid down any high balances, shoot for keeping your credit utilization under 10%.

It will boost your credit profile, and make it easy to keep your debt and monthly payments under control.

Pay off credit card balances in full whenever possible. By paying off your balance each month, you’ll master your credit and avoid interest charges. That payment history will boost your score, and keep you in control of your budget.

Avoid credit inquiries. Remember, the more applications you make for new credit, the less attractive you seem as a borrower. Limit your applications when you’re in the credit building process, and it’ll help your credit profile long-term.

Be credit smart. Get educated on credit – this is a great place to start! Keep an eye out for changes in legislation related to consumer credit and stay focused on your goal. You’ll be leveling up in no time!

Wrapping Up

Have you been working on your credit? What improvements have you made since you became credit-focused?

Share your success stories in the comments!

Use the resource below to check your credit report and get a snapshot of your FICO score.

CreditScorecard.com – Offers an Experian FICO score once each month. Sponsored by Discover.

Use the resources below to check your credit reports and get a snapshot of your VantageScore.

CreditKarma.com – Provides an updated VantageScore weekly.

WalletHub.com – Provides an updated VantageScore monthly.

AnnualCreditReport.com: Check your credit report from each bureau for free.

Credit Score Tracker: A digital print out where you can chart your credit progress as your score grows.

Want more content like this? Subscribe now to get access to our original shows, in-depth guides, courses, and exclusive experiences.

Grab your Breadwinner Journal & level up your money mindset!

TOOLS

Journals

Planners

Affirmation Decks

FREE RESOURSES

Podcasts

Abundant! Mantra

Master Account List

Spending Tracker

Take this free quiz to discover

your money strengths

and embrace financial self-confidence.

Terms & Conditions | Privacy Policy | Affiliate Disclosure | Contact Us